To make “The upcoming deal” free for readers, we earn cash from advertisers, together with monetary professionals and corporations that pay to be featured. This creates a battle of curiosity after we favor their promotion over others. Learn our editorial coverage and phrases of service to be taught extra. “The upcoming deal” just isn’t a shopper of those monetary companies suppliers.

➡️ Discover a Native Advisor | 🎯 Discover a Specialist Advisor

In accordance with a February 2022 report printed by the Federal Reserve of New York, excellent bank card balances within the US grew by $52 billion on the finish of 2021, a report quarterly improve.

Should you’re among the many hundreds of thousands of Individuals feeling pinched by larger minimal month-to-month funds, there are three steps you may take to rapidly scale back your debt and the stress that comes with it. That is particularly welcome information since almost certainly the debt isn’t even your fault.

Overspending does occur, nevertheless it’s not the one trigger for credit-card debt. Emergency bills (e.g., medical payments, auto repairs, and many others.), job loss, and/or divorce, pull numerous households right into a debt spiral. Regardless of how you bought there, what’s an individual to do?

First, Some Historical past

Bank cards’ roots go all the way in which to historical Mesopotamia, the place clay tablets have been used to facilitate commerce. The primary recognizable cost card was the “Charg-It card,” provided by Brooklyn banker John Briggins financial institution. The primary Diner’s Membership card got here out in 1949; adopted by American Categorical providing the primary common cost card in 1959. Financial institution of America’s BankAmericard®, first provided in 1966, was the primary to permit revolving credit score. Every of those evolutionary steps made credit score a extra handy, highly effective software. It additionally made bank card debt nearly inevitable.

If that’s your present state of affairs, right here’s what it’s essential do…

If You Discover Your self in a Gap – First, Cease Digging!

It’s form of apparent, besides should you’re the one within the gap.

It’ll by no means get any simpler to dig out should you preserve going the way in which you’ve got so far. So, earlier than we get to methods of digging out of excessive bank card debt, cease digging your self deeper.

Minimize your spending so that you’re not including to your debt.

- For every buy, ask your self, “Do I really want this?”

- If sure, ask your self, “Can I delay the acquisition?”

- Should you can’t, ask your self, “Is there a less expensive various?”

- No matter your solutions to the above, arrange reminders to pay on time a minimum of the minimal for every card to keep away from late-payment charges and penalty rates of interest.

Bear in mind the large price of bank card debt. For instance, say you owe $5000 on a 14% APR card, $1000 on a 20% APR card, and $4000 on a 24% APR card. And lest you say that is an unrealistic instance, in accordance with NerdWallet, the typical American family with bank card debt owes over $6000 and pays a mean of $1029 a 12 months in bank card curiosity. The common annual curiosity price within the above instance is lower than $850.

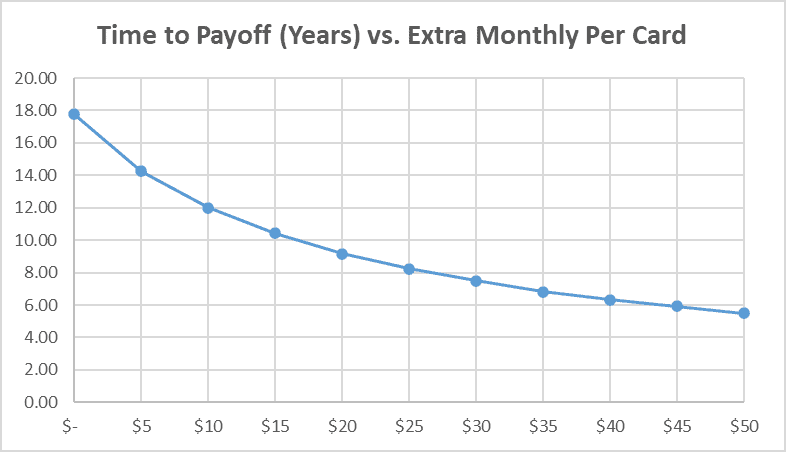

Should you cost nothing else and make solely the minimal funds on every card, that $10,000 debt will price you over $12,500 in curiosity, and take practically 18 years to repay.

First Strategy to Dig Out – Scale back Your Curiosity Fee to Speed up Payoff

For the reason that supply of ache of bank card debt is their excessive rate of interest, decreasing that curiosity is your high precedence. You’ve got three choices right here:

- Contact your card issuer(s) and ask for an interest-rate discount. Should you’re a great longtime buyer, they might agree fairly than lose you to a different lender.

- Consolidate your debt with a peer-to-peer mortgage (Lending Membership, Prosper, and many others.) at a aggressive APR.

- Consolidate your debt with an 18-24 month 0%-APR steadiness switch supply (see e.g. Bankrate, Nerdwallet, or Wallethub). As of late, such provides include a 3-5% price, however could supply a $200 bonus.

Let’s consider the final possibility, because it’s possible greatest for most individuals.

In our instance, switch all of your card debt to a brand new card at 0% APR for 18 months, a 3% price, and a $200 bonus after 3 months of well timed funds, and in 18 months your debt will drop by practically half.

Rinse and repeat, and after one other 18 months, your debt will drop to $377. Even at 20% APR, you may pay this off in simply 2 extra months.

Your whole price right here, together with the three% steadiness switch charges, is a mere $64; and your time to debt freedom is simply over 3 years. This protects you 99.5% of your curiosity price vs. paying simply the minimal, and will get you out of debt 5x sooner!

Even with out the $200 bonus you’d save 98% of curiosity and take only one month extra to get out of debt.

“Contemplate a debt consolidation mortgage should you can solely afford to pay the minimal (or simply over the minimal), in case your bank cards all carry a high-interest fee, and your credit score rating is a minimum of 600,” says Blaine Thiederman, CFP. “Search for consolidation mortgage suppliers that cost a minimal origination price (if any in any respect),” Thiederman says.

Second Strategy to Dig Out of Excessive Credit score Card Debt – Pay Greater than the Minimal

It’s arduous. I do know.

You wrestle to make ends meet whereas paying simply the minimal on every card. Including even somewhat to every card fee appears unimaginable.

However should you can’t get authorized for any of the above consolidations or interest-rate reductions, the next path can nonetheless prevent hundreds of {dollars} and years off your journey out of debt.

As you may see within the graphs under, should you pay as little as $5 a month further to every card, you’ll save over $2350 and three.5 years in debt.

$10 a month per card would prevent over $3900 and practically 6 years.

$20 a month per card would minimize your curiosity by $5850 and your time to closing payoff by over 8.5 years.

$50 a month per card, and also you slash practically $8500 and 12 years – over 2/3 of each curiosity paid and time.

One vital observe right here is that as you narrow down your balances, your minimal funds drop too, making it simpler to maintain digging out.

Third, Optimize Your Card Funds

Within the above instance, including simply $15 ($5/card) to your month-to-month funds, for a complete of $270/month, saves you $2350 and three.5 years in debt. However you may optimize and minimize much more!

First, preserve paying the identical $270 regardless of your minimal required funds steadily reducing.

Second, use the “Snowball Methodology,” advocated by debt-busting guru Dave Ramsey.

Right here, you ship simply the minimal to all however the lowest-balance card. To that one, ship the distinction between your $270 whole and people different minimums. When you repay that card, goal the subsequent lowest steadiness card. When you pay that off too, ship the total $270 to the ultimate card.

This methodology would prevent over $5300 greater than the $2350+ financial savings of the earlier methodology. It additionally will get you out of debt nearly a decade earlier!

Should you can keep the course it doesn’t matter what, use the Avalanche Methodology. It really works just like the Snowball Methodology, besides that it targets bank cards in descending order of rate of interest. In our instance, this protects you $180 and an additional month greater than the Snowball Methodology.

Use Free On-line Sources

You may as well discover useful web sites and on-line instruments that will help you develop a method to repay your bank cards and monitor your progress. Along with dozens of debt discount blogs that provide methods and help for his or her readers, one useful resource really helpful by monetary consultants is PowerPay, a software created by Utah State College.

“Use PowerPay so you may see the sunshine on the finish of your debt tunnel,” says Maggie Klokkenga, proprietor of Make a Cash Mindshift. “PowerPay is a free on-line debt fee calculator the place you may enter all your debt, and the calculator will present the alternative ways that you would be able to pay down the debt, for instance, lowest steadiness first (debt snowball) or highest curiosity first (debt avalanche),” says Klokkenga.

Keep away from Temptation

In fact, to efficiently repay your bank cards, you will have to keep away from accumulating further debt. With on-line purchasing transactions all the time only a click on or two away, contemplate steps you may take to scale back the temptation.

“One trick to getting folks over the bank card hump is to make it arduous to make use of the cardboard and all types of it, together with on-line kinds which are actually so simply saved on web sites,” says Terri Bailey of Higher Monetary Counseling. “My advice is to take apps off your cellphone, don’t bodily carry playing cards, and keep off of your set off web sites,” says Bailey.

The Backside Line

Should you’re deep in bank card debt, your first and speedy concern is to cease digging your self deeper.

Subsequent, consolidating your debt utilizing a long-term 0%-APR steadiness switch supply (even with a 3% price) may prevent nearly all curiosity price and get you out of debt quick.

If that’s not an possibility, chopping bills even somewhat and bumping your funds over the minimal can prevent hundreds of {dollars} and years of debt servitude. Use the Snowball or Avalanche strategies to avoid wasting way more in each time and money.

—

Supply: New York Fed Family Credit score Examine

Are you able to get pleasure from life extra with much less cash stress?

Signal as much as obtain weekly insights from “The upcoming deal” with helpful cash suggestions and recent concepts that will help you obtain your monetary targets.

Disclaimer: This text is meant for informational functions solely, and shouldn’t be thought of monetary recommendation. It’s best to seek the advice of a monetary skilled earlier than making any main monetary selections.